All Life Insurance is “Whole Life”

Updated on June 14, 2022

Have you ever heard of whole life insurance? In most situations, it’s a generic word that’s meant to describe a permanent insurance policy. And in previous years, the industry has commonly separated life insurance between two categories: temporary and permanent. What if we told you that with the evolution of insurance products, the line between them has blurred, and now all life insurance (temporary and permanent) is whole life. Confused yet?

Well, we don’t want you to be. Cove is taking the lead in modernizing the approach to how advisors and consumers think and talk about life insurance products to reflect the new paradigm that “All Life Insurance is Whole Life”.

Now, what do we mean when we say all life insurance is whole life? This means that, as long as premiums are paid, the life insurance policy will be in place for the whole of the insured’s life. This is important when the life insurance need doesn’t go away such as when needed for funding capital gains taxes, equalizing estate values for multiple beneficiaries, or providing for a charity.

We wanted to move away from distinguishing life insurance between term insurance and permanent insurance because these names don’t tell the entire story and don’t provide the client with any further information other than the fact that it’s life insurance.

So if we acknowledge that all life insurance is whole life, how can we distinguish them from one another? We have done many hours of thinking and research to find the answer to this question. What we feel is best for the industry, for clients, and for insurance advisors is to start separating products by what they offer and not by the name given to it by the industry.

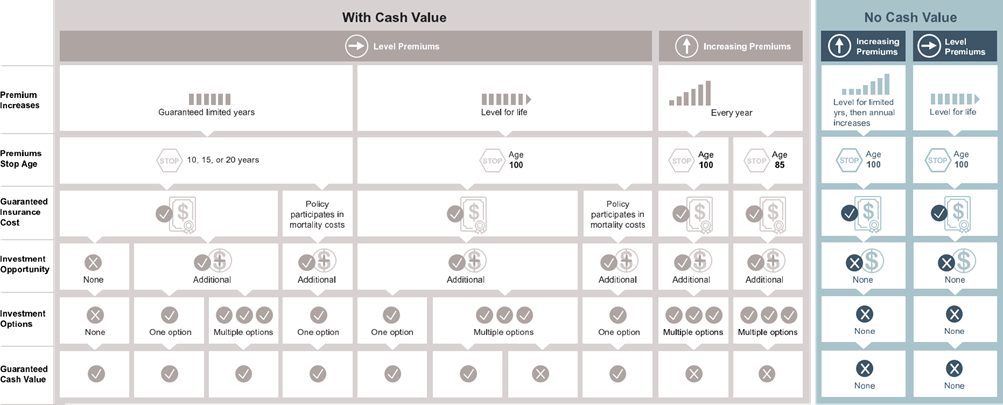

Thus, we have separated the products into two categories:

- Policies with a Cash Value

- Policies without a Cash Value

And within a cash value policy, there are three sub-types:

- Guaranteed cash value only

- Variable cash value only

- Both guaranteed and variable cash value

In doing so, we immediately isolate those products that can provide life insurance only and can contrast those with a policy that may have a higher premium but offers an opportunity for guaranteed cash values or an opportunity to create cash values.

But this is just one of the client’s steps in choosing an insurance plan design that best suits their situation. It’s not an ‘A’ or ‘B’ decision, and that’s why life insurance is more nuanced than just choosing between “term life insurance” and “permanent life insurance”. It’s about looking at all the plan design components and selecting the preferred option for the client. Here are a few plan design components for consideration.

Level Premiums vs Increasing Premium

Premium for Lifetime vs Premium for Limited Number of Years

Guaranteed Insurance Cost vs a Policy that Participates in the Insurance Company’s Mortality Costs

Option for Investment Deposits vs No Option for Investment Deposits

Multiple Investment Options vs One Investment Option

When someone with life insurance dies, the beneficiary doesn’t typically care what kind of insurance policy it was or the special features the insurance had. They mostly care about the insurance money showing up when it is supposed to. All life insurance is the same in that when the insured dies, the benefit is paid.

But how the policy operates, what it offers or what it does for the insured during their lifetime is important. This is why we all must focus on the plan design, and not the industry-given name when choosing a life insurance product.

Although there are numerous things to consider, the process of choosing the right plan is relatively simple. At Cove, we have developed tools to boil down the options into simple fundamentals for you to understand.

With over 30 years of experience analyzing and testing products and applications, plus working with insurance company actuaries on product development and seeing firsthand what does and doesn’t work, we can guide you through the decision-making process, so you can feel fully confident in choosing the best life insurance plan design for yourself.

Book a meeting with one of our advisors to learn how we can provide an insurance plan design that suits your needs.

No Comments

Sorry, the comment form is closed at this time.